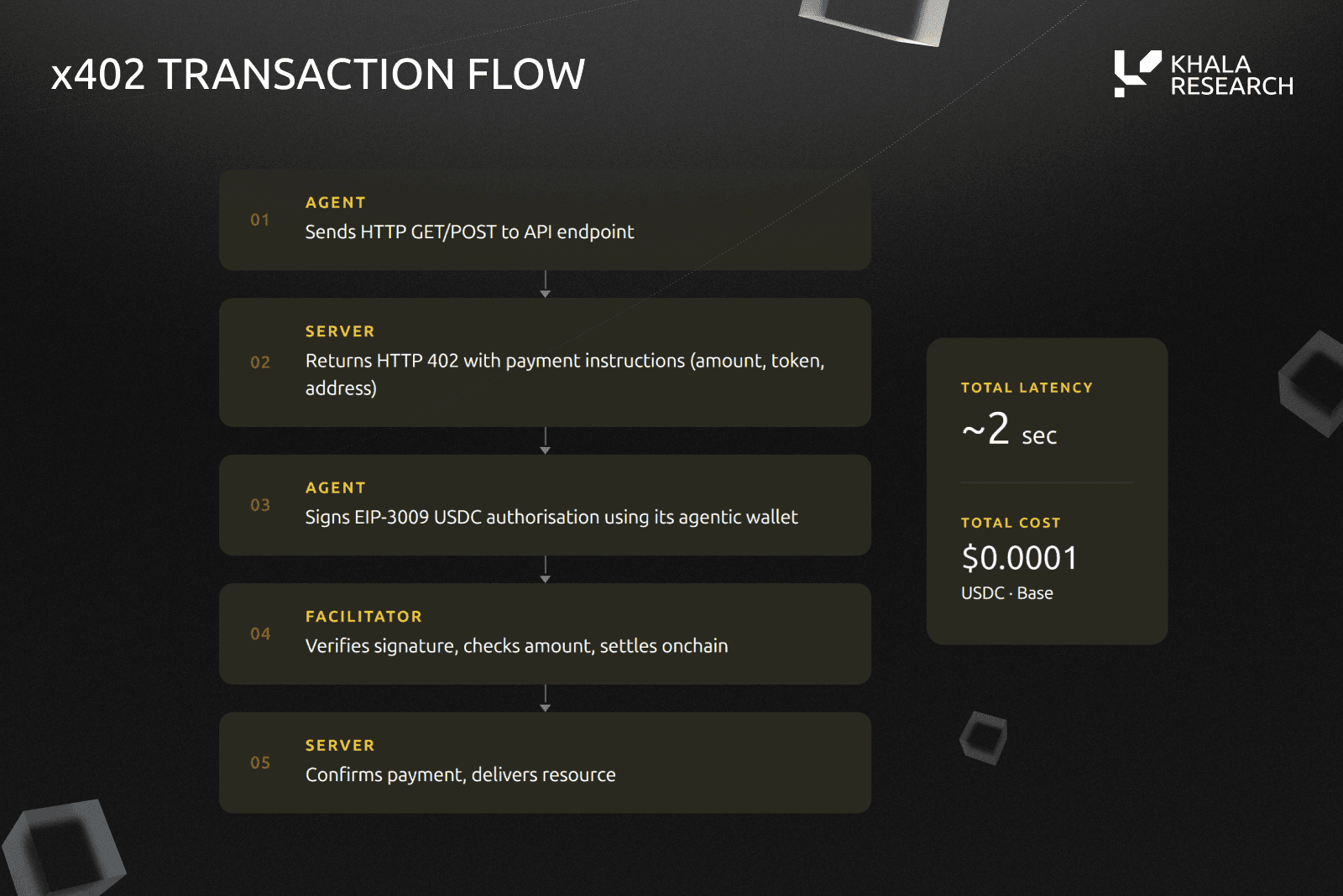

Set up x402 payment middleware

To route KYC or AML checks through an x402-enabled API, install the necessary dependencies and configure the payment gateway to handle HTTP 402 responses. This middleware acts as the gatekeeper, ensuring compliance verification happens at the infrastructure level rather than inside your business logic. By intercepting the response early, you prevent unauthorized access to protected endpoints and keep your core application clean.

Start by installing the official x402 middleware package for your runtime environment. This package provides the foundational hooks needed to detect when a client needs to pay for a service. It also handles the initial handshake with the payment provider, ensuring that the transaction is valid before any sensitive customer data is exposed.

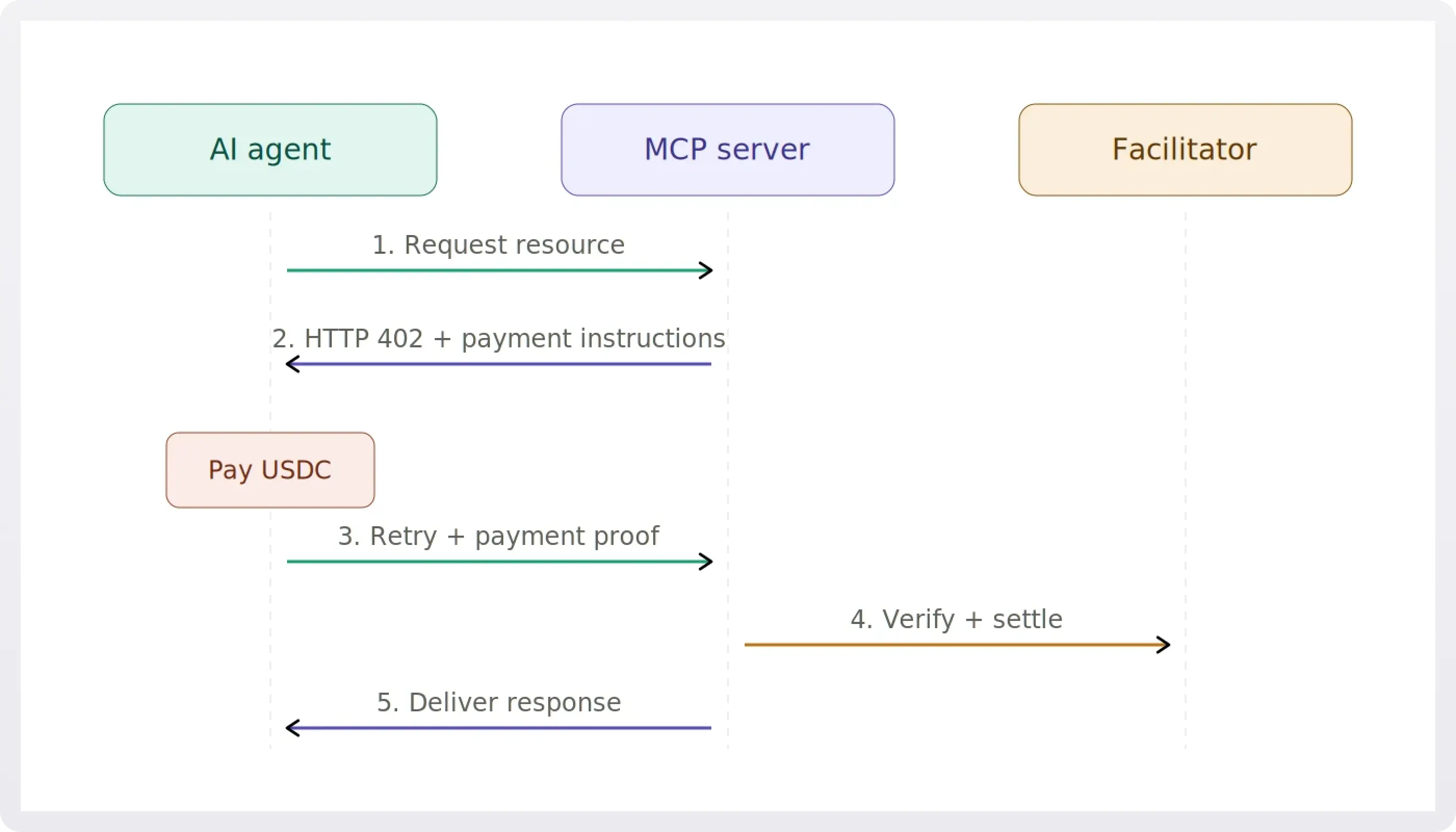

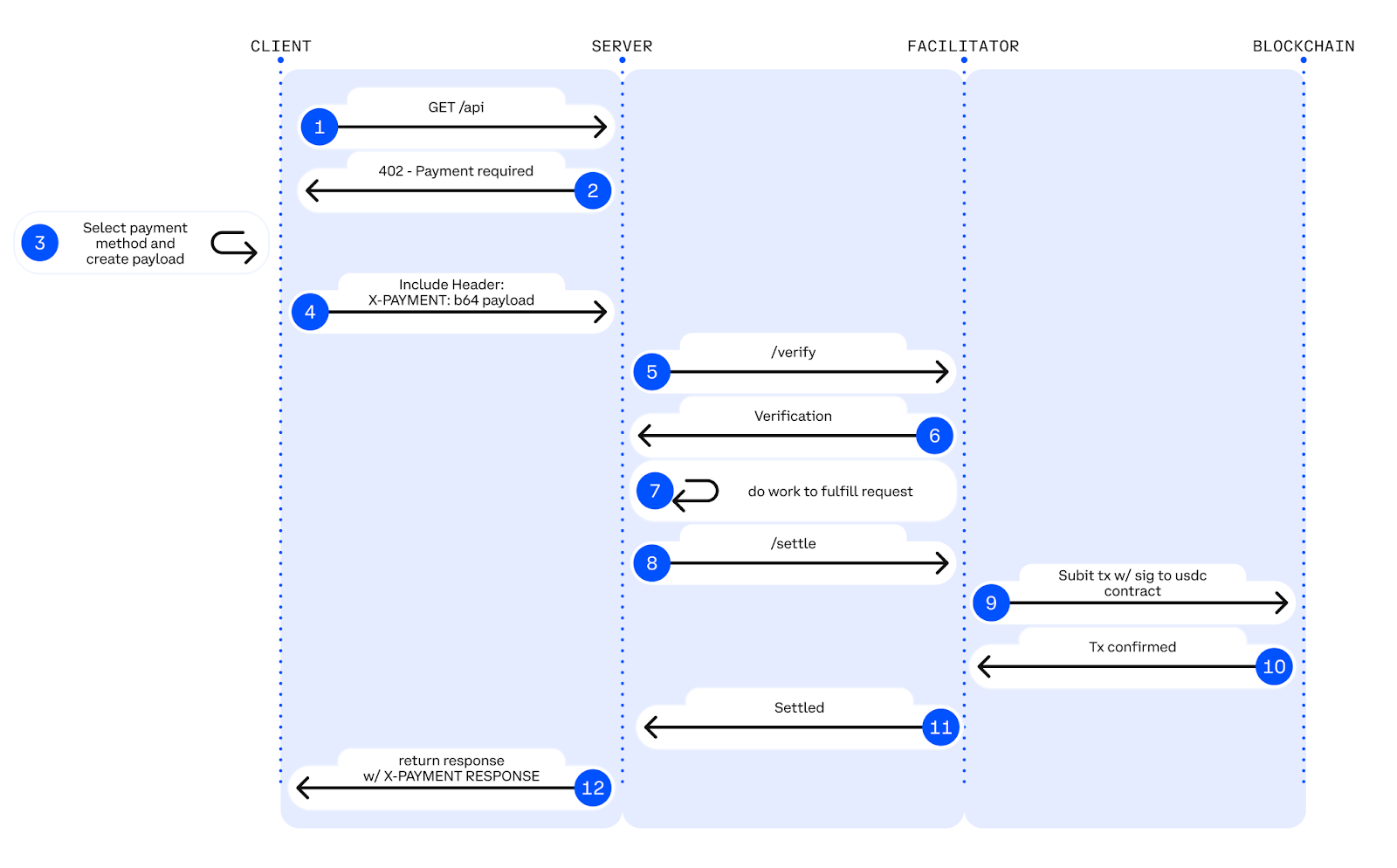

Next, configure the middleware to return a 402 Payment Required status when a request lacks valid proof of payment or compliance. This is not an error; it is a signal. The middleware should include a Payment-Required header that specifies the cost and the payment method. This allows clients, including automated agents, to understand exactly what is needed to proceed.

Once the middleware is active, test it with a simple endpoint that requires payment. Verify that the 402 response includes all necessary headers and that the client can successfully complete the transaction. This setup ensures that your KYC/AML checks are backed by a verified payment, adding a layer of trust and accountability to your API.

Integrate KYC verification logic

To embed KYC/AML checks into your x402 API flow, treat identity verification as a gatekeeper before any payment or service delivery occurs. The x402 protocol allows you to attach payment logic directly to API responses, but it does not inherently handle regulatory compliance. This means your application must validate that the user has passed their KYC checks before the payment token is issued or the endpoint is accessed.

The integration relies on a simple sequence: verify identity, validate compliance status, and then trigger the x402 payment response. You can use zero-knowledge proofs (ZKPs) to prove compliance without exposing sensitive personal data, a feature supported by networks like Concordium [src-serp-2]. This approach keeps your API efficient while satisfying regulatory requirements for customer identification and transaction monitoring [src-serp-4].

1. Install and configure verification dependencies

Before writing any logic, ensure your environment has the necessary SDKs for both KYC verification and x402 payment handling. Install the provider-specific SDKs (e.g., for identity verification) and the x402 client library. Configure your environment variables with API keys for the KYC provider and your x402-enabled wallet or node. This setup ensures your backend can communicate with both the identity provider and the payment network simultaneously.

Initialize the KYC provider's SDK in your backend. This usually involves creating a client instance with your API credentials. Ensure the SDK is configured to handle the specific verification method you are using, such as document upload or biometric scan. This step establishes the connection between your app and the identity verification service.

2. Implement identity collection and submission

When a user attempts to access a regulated endpoint, your API should first check if they have an existing KYC record. If not, redirect them to a verification flow. Collect the necessary data—such as government ID, selfie, or address proof—and submit it to your KYC provider. Do not store this sensitive data locally unless absolutely necessary; rely on the provider's secure storage and return a verification token or status ID.

Build a secure form or API endpoint to collect user identity documents. Use encryption in transit and at rest if you must store temporary data. Submit this data to your KYC provider's verification endpoint. The provider will return a unique verification ID or a status (e.g., "pending," "verified," "rejected") that you will use in the next step.

3. Validate compliance status before x402 trigger

Once the KYC provider returns a status, your backend must validate it. This is the critical gate. If the status is not "verified," your API should return a 403 Forbidden or a specific error code indicating compliance failure. Do not proceed to the x402 payment logic. If the status is "verified," proceed to generate the payment token. This ensures that no payment is processed for unverified users, keeping your service compliant with AML regulations.

Query your KYC provider's status endpoint using the verification ID. Parse the response to confirm the user is "verified." If the status is pending, you may choose to hold the request or require additional steps. Only when the status is explicitly "verified" should you allow the flow to continue to the x402 payment generation step.

4. Generate and return the payment token

With compliance confirmed, your backend can now generate the x402 payment token. This token is attached to the API response, effectively granting the user access to the service. The token should include the payment amount, the recipient address, and any metadata required by your x402 implementation. Return this token to the client, which can then use it to complete the transaction or access the service.

Use your x402 client library to create a payment token. This token is cryptographically signed and contains the payment details. Attach this token to your API response. The client can then use this token to pay for the service or access the endpoint. This step completes the integration, ensuring that payment and compliance are handled in a single, secure flow.

5. Implement ongoing monitoring and re-verification

KYC/AML compliance is not a one-time event. Implement logic to monitor for changes in user risk profiles or regulatory status. If a user's KYC status changes (e.g., they are flagged for suspicious activity), your API should automatically revoke their x402 access. Set up periodic re-verification checks, especially for high-value transactions or high-risk users. This ensures that your service remains compliant over time, not just at the point of entry.

Configure webhooks or scheduled jobs to monitor user KYC status. If a user's status changes to "flagged" or "expired," update your internal records and revoke their x402 access. Implement periodic re-verification prompts for high-risk users. This proactive approach helps you stay compliant with ongoing AML requirements and reduces the risk of financial crime.

6. Test the integration with compliance scenarios

Before deploying, test your integration with various KYC scenarios: successful verification, rejection, pending status, and expired credentials. Ensure that your API correctly blocks access for non-verified users and allows access for verified ones. Test edge cases, such as network timeouts or provider outages, to ensure your system handles errors gracefully. This testing phase is crucial for identifying any gaps in your compliance logic before they impact real users.

Create test cases for each KYC status: verified, rejected, pending, and expired. Verify that your API returns the correct responses for each case. Test error handling for provider outages. Ensure that your system logs all compliance-related events for audit purposes. This thorough testing ensures that your integration is robust and compliant under all conditions.

7. Document and audit your compliance flow

Finally, document your KYC/AML integration process. This documentation should include the steps taken to verify identity, how compliance status is checked, and how payment tokens are generated. This documentation is essential for internal audits and regulatory reviews. Ensure that your logs capture all relevant data points, such as verification IDs, timestamps, and token generation events. This creates a clear audit trail that demonstrates your commitment to compliance.

Write detailed documentation of your KYC/AML integration. Include diagrams of the data flow and code snippets for key functions. Ensure that your logs capture all compliance-related events. This documentation is essential for internal audits and regulatory reviews. It demonstrates your commitment to compliance and helps you quickly respond to any regulatory inquiries.

Structure payment schemes for access

You can monetize KYC and AML checks through x402 using two primary billing models: fixed pricing or dynamic, metered pricing. Your choice depends on whether your compliance checks have a predictable scope or fluctuate based on user risk profiles.

Fixed pricing for standard checks

Fixed pricing assigns a set cost to each verification type, such as a standard identity check or a basic sanctions list search. This model is straightforward for developers to implement and for users to budget for. You define the price in the x402 response header, and the client pays that exact amount regardless of the underlying computational cost.

This approach works best for routine, low-complexity checks where the risk profile is stable. It simplifies the integration logic because you do not need to track usage metrics or calculate variable fees per transaction. Users appreciate the transparency, knowing exactly what a check costs before they initiate it.

Dynamic pricing for complex verification

Dynamic pricing adjusts the fee based on the depth of the verification. For example, a basic name match might cost less than a full enhanced due diligence (EDD) check that includes adverse media scanning and source of funds verification. This model aligns the cost with the value and complexity of the service provided.

Implementing dynamic pricing requires your API to calculate the fee in real-time based on the specific checks requested. The x402 protocol supports this by allowing you to return a variable Payment-Required header that reflects the current cost. This ensures that high-risk customers who require more thorough screening pay a fair price that covers the additional compliance overhead.

Choosing the right model

The decision between fixed and dynamic pricing should be driven by your compliance requirements and user experience goals. Fixed pricing is easier to manage and predict, making it ideal for simple onboarding flows. Dynamic pricing is more flexible and accurate for complex financial services where risk varies significantly.

Consider starting with fixed pricing for standard checks to keep integration simple. You can layer in dynamic pricing for specialized or high-risk checks as your platform matures. This hybrid approach allows you to balance ease of use with accurate cost recovery for complex compliance tasks.

| Feature | Fixed Pricing | Dynamic Pricing |

|---|---|---|

| Cost Predictability | High | Variable |

| Implementation Complexity | Low | High |

| Best Use Case | Standard KYC | Enhanced Due Diligence |

| Revenue Alignment | Static | Risk-Based |

Comparison of Payment Schemes for KYC/AML

Choosing the right payment scheme for x402 endpoints requires balancing implementation speed, transaction costs, and regulatory coverage. While the underlying mechanism is similar, the nuances of each protocol affect how quickly you can go live and how much you pay per check.

Stripe Connect

Stripe offers the most mature integration path for developers. Their API handles most of the heavy lifting for KYC data collection, reducing your compliance burden. However, fees are higher, typically around 2.9% + 30¢ per transaction. This scheme is best for established businesses prioritizing stability over cost.

Coinbase Commerce

Coinbase provides a lower-cost alternative with simpler integration requirements. The API is straightforward, but you must handle more of the KYC/AML logic yourself to ensure compliance. Transaction fees are significantly lower, making it attractive for high-volume, low-margin checks. This is ideal for developers comfortable managing their own compliance workflows.

PayPal Payouts

PayPal is a familiar option with broad user adoption. Integration is moderate, requiring careful handling of international regulations. Fees are competitive but can vary by region. This scheme works well for services targeting global audiences where PayPal is the preferred payment method, though it may require additional compliance steps for cross-border AML checks.

Summary Table

| Scheme | Dev Complexity | Avg. Cost | Compliance Coverage |

|---|---|---|---|

| Stripe Connect | Low | 2.9% + 30¢ | High |

| Coinbase Commerce | Medium | ~1% | Medium |

| PayPal Payouts | Medium | Variable | High |

Technical trends show a steady increase in x402-enabled compliance API usage, reflecting the growing demand for seamless, payment-gated identity verification. The following chart illustrates this volume growth over the last quarter.

No comments yet. Be the first to share your thoughts!