Why agent commerce needs x402 compliance

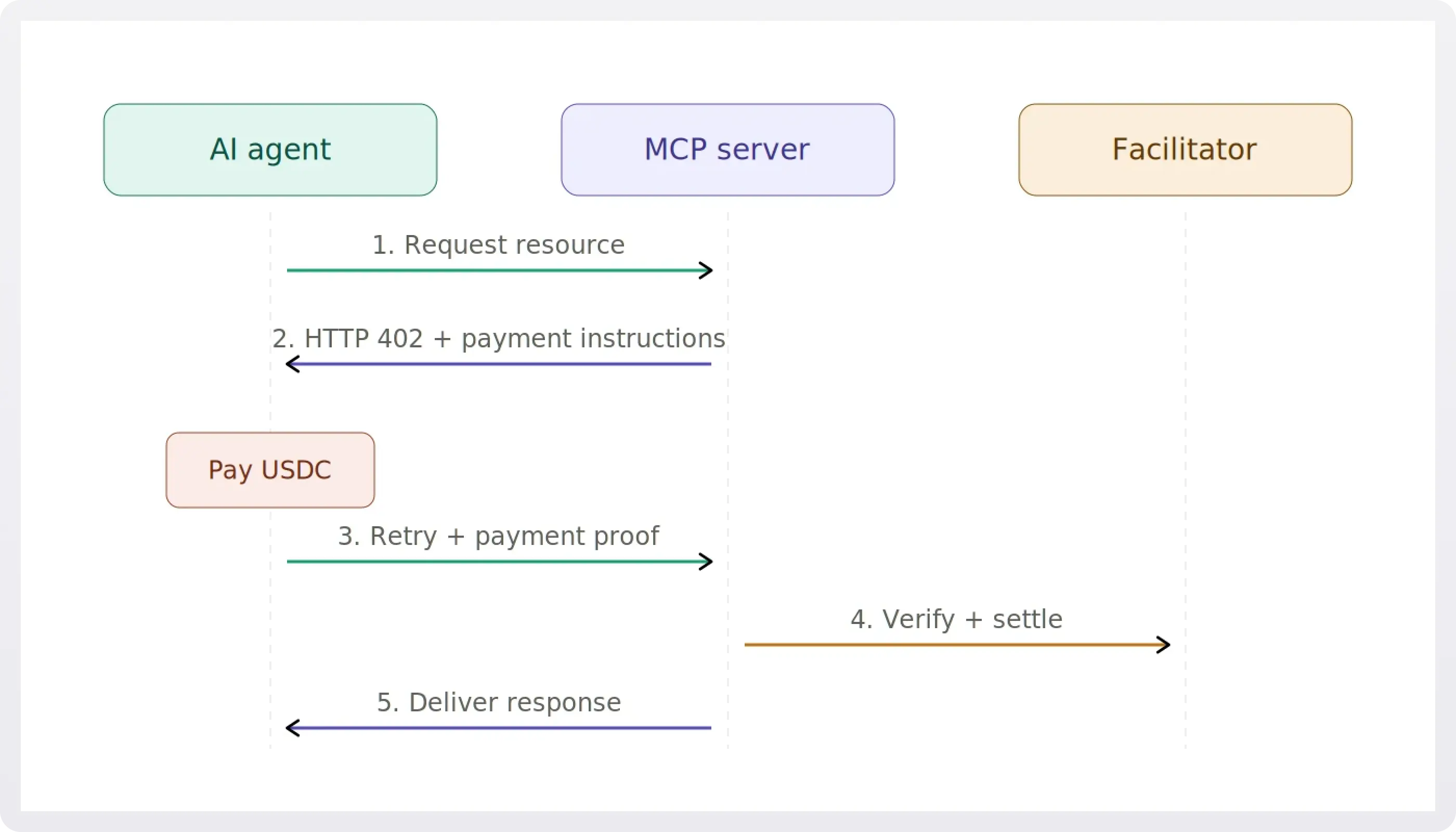

Autonomous agents operate at machine speed, but regulatory frameworks move at human speed. When an AI agent initiates a payment via the x402 protocol, it triggers a financial transaction that must satisfy legal obligations. The x402 standard enables machine-to-machine payments by returning an HTTP 402 status code with a URI for payment. However, this mechanism alone does not verify the identity of the payer or the legitimacy of the funds.

x402 enables machine-to-machine payments, but regulatory frameworks still require identity verification for high-value or high-risk transactions.

Without integrated KYC/AML layers, an agent commerce infrastructure risks facilitating money laundering or sanctions violations. Standard HTTP 402 integration is insufficient for compliance because it focuses on settlement, not verification. Legal frameworks, such as those discussed by Braumiller Law, emphasize that stablecoin payments require clear identity attribution to meet anti-money laundering standards.

Integrating compliance checks directly into the x402 flow ensures that agents only transact with verified entities. This alignment between automated payments and regulatory requirements is essential for sustainable agent commerce.

How x402 Payments Work

The x402 protocol transforms standard HTTP requests into verifiable financial transactions. Instead of relying on a third-party payment processor to hold funds, x402 embeds the payment directly into the API response. This architecture creates a closed loop where the service provider receives payment only after delivering the requested data or service, and the buyer receives cryptographic proof that the transaction occurred.

At the center of this system is the PaymentPayload. When an agent or application requests a KYC/AML check, the x402 client constructs a payload containing the payment details and the specific service parameters. This payload is signed by the buyer using their private key. This signature is critical for compliance because it creates an immutable, non-repudiable record of intent. The buyer cannot later claim they did not authorize the payment, and the provider cannot claim they did not receive it.

Settlement happens directly on-chain. Once the payload is sent, the blockchain network validates the signature and transfers the stablecoin value to the provider’s wallet. This on-chain settlement ensures that the audit trail is public, transparent, and resistant to tampering. For legal and regulatory frameworks, this means every transaction is tied to a specific block height and wallet address, simplifying the process of tracking fund flows and verifying compliance.

This direct settlement model removes the need for escrow services or complex reconciliation processes. The buyer’s signature serves as the contract, and the blockchain serves as the ledger. This reduces friction in agent-commerce interactions, allowing high-volume, low-value checks to occur without the overhead of traditional banking rails.

KYC/AML integration patterns for APIs

Embedding KYC/AML checks into x402 endpoints requires more than a simple identity verification gate. Because x402 enables machine-to-machine payments, the compliance logic must be programmatically enforceable at the protocol level. This means integrating screening directly into the payment flow rather than treating it as an afterthought.

There are three primary integration patterns for embedding these checks into API endpoints:

| Pattern | Timing | Use Case | Risk Level |

|---|---|---|---|

| Pre-Transaction Screening | Before payment authorization | High-value B2B agent commerce | High |

| Post-Transaction Monitoring | After payment settlement | Low-value microtransactions | Medium |

| Risk-Based Authentication | Dynamic, based on score | Variable risk agent interactions | Variable |

Pre-transaction screening

This pattern verifies identity and sanctions status before the x402 endpoint authorizes a payment. It is the most robust approach for high-value transactions where regulatory exposure is significant. The endpoint rejects the request immediately if the counterparty fails the check, preventing the transaction from occurring.

Post-transaction monitoring

For low-value, high-volume microtransactions, pre-screening can introduce unacceptable latency. In this pattern, the x402 endpoint processes the payment first, then flags the transaction for review. Suspicious activity is reported to compliance teams after the fact, balancing speed with regulatory oversight.

Risk-based authentication

This dynamic approach adjusts the verification depth based on real-time risk scores. An x402 endpoint might skip full KYC for trusted, low-risk agents while triggering enhanced due diligence for new or high-risk counterparts. This pattern requires sophisticated risk scoring engines integrated into the API logic.

Choosing the right pattern depends on your transaction volume, average value, and regulatory jurisdiction. Pre-transaction screening offers the strongest compliance posture, while post-transaction monitoring prioritizes user experience. Risk-based authentication provides a balanced middle ground, adapting to the specific context of each agent interaction.

Implementing x402 Endpoints for KYC/AML Checks

Integrating x402 with KYC/AML verification requires a structured approach to handle compliance data and crypto payments simultaneously. The goal is to ensure that every transaction triggers the necessary identity checks before funds are released or services are accessed.

Start by selecting a compliant provider such as Sumsub or Onfido. Register your API keys in a secure environment variable. This step establishes the foundation for all subsequent identity verification requests. Ensure the provider supports webhook notifications for real-time status updates.

Create a dedicated API route that handles the x402 payment intent. This endpoint must validate the incoming cryptocurrency payment and generate a unique session ID. The session ID links the payment to the specific user’s KYC record. Use the Coinbase Developer Platform documentation to ensure your payload structure matches the protocol standards.

When a user initiates a transaction, your backend should automatically trigger a KYC check. Pass the user’s unique identifier and the x402 session ID to your provider’s API. This creates a direct correlation between the financial transaction and the identity verification process. The provider will return a verification status that your system must monitor.

Set up a webhook listener to receive real-time updates from your KYC/AML provider. If the verification fails, reject the x402 payment request immediately. If it passes, update the user’s session state to allow access to the service. This ensures that only verified users can complete transactions, reducing regulatory risk.

Run a full integration test using sandbox credentials from both your x402 provider and your KYC vendor. Verify that payments are only processed after successful identity checks. Check that failed verifications correctly block transaction completion. This step confirms that your compliance logic is robust and ready for production.

Regulatory risks and mitigation strategies

Agent-commerce introduces unique friction points where automated agents handle sensitive identity data and financial settlements. The primary risk lies in the ambiguity of liability when an agent facilitates a transaction that later triggers a regulatory violation. Unlike traditional human-mediated commerce, the "facilitator" is code, making it difficult to assign fault when data privacy standards are breached or when anti-money laundering (AML) checks fail.

To mitigate these risks, developers must treat KYC/AML checks not as optional add-ons but as foundational infrastructure. This means embedding verification steps directly into the x402 payment flow, ensuring that compliance is a prerequisite for service access rather than an afterthought. Relying on third-party summaries is insufficient; you must reference official regulatory texts and primary documentation to ensure your agents are interpreting compliance requirements correctly.

Jurisdictional compliance is another critical hurdle. Agents operating across borders must navigate conflicting data privacy laws, such as the GDPR in Europe or CCPA in California. A robust mitigation strategy involves geo-fencing sensitive operations and using provider-backed tools to monitor regulatory changes in real-time. This proactive approach reduces the likelihood of costly fines and builds trust with users who expect their data to be handled with legal precision.

Frequently asked questions about x402 compliance

Does x402 replace KYC/AML checks?

No. x402 provides the technical infrastructure for agent-to-agent commerce, but it does not perform identity verification. Compliance remains the responsibility of the service providers integrating the protocol. As noted by Fenergo, KYC and AML compliance involves verifying customer identities and monitoring transactions, which happens before or alongside the x402 payment flow rather than inside it.

How does x402 handle suspicious activity reporting?

x402 PaymentPayloads are signed by the buyer and settled directly onchain, creating an immutable audit trail. This transparency allows compliance teams to trace funds and detect anomalies more easily than with opaque traditional gateways. However, the protocol itself does not automatically flag or report suspicious activity; that logic must be implemented by the integrating agent or compliance layer.

Is x402 compliant with global financial regulations?

x402 is a protocol standard, not a legal entity, so it cannot be "compliant" in isolation. Its onchain nature aligns with regulatory preferences for transparency and auditability. Integrators must ensure their specific implementation meets local requirements, such as the Travel Rule for cross-border transactions or FATF guidelines for virtual asset service providers.

No comments yet. Be the first to share your thoughts!