Why agent commerce needs compliant payments

AI agents are no longer just drafting emails; they are moving money. When an autonomous agent negotiates a contract and settles it with a stablecoin, the transaction happens at machine speed. This creates a compliance paradox: financial regulations like KYC and AML require human-level due diligence, but agents operate in milliseconds. Without a protocol-level solution, this friction breaks the model.

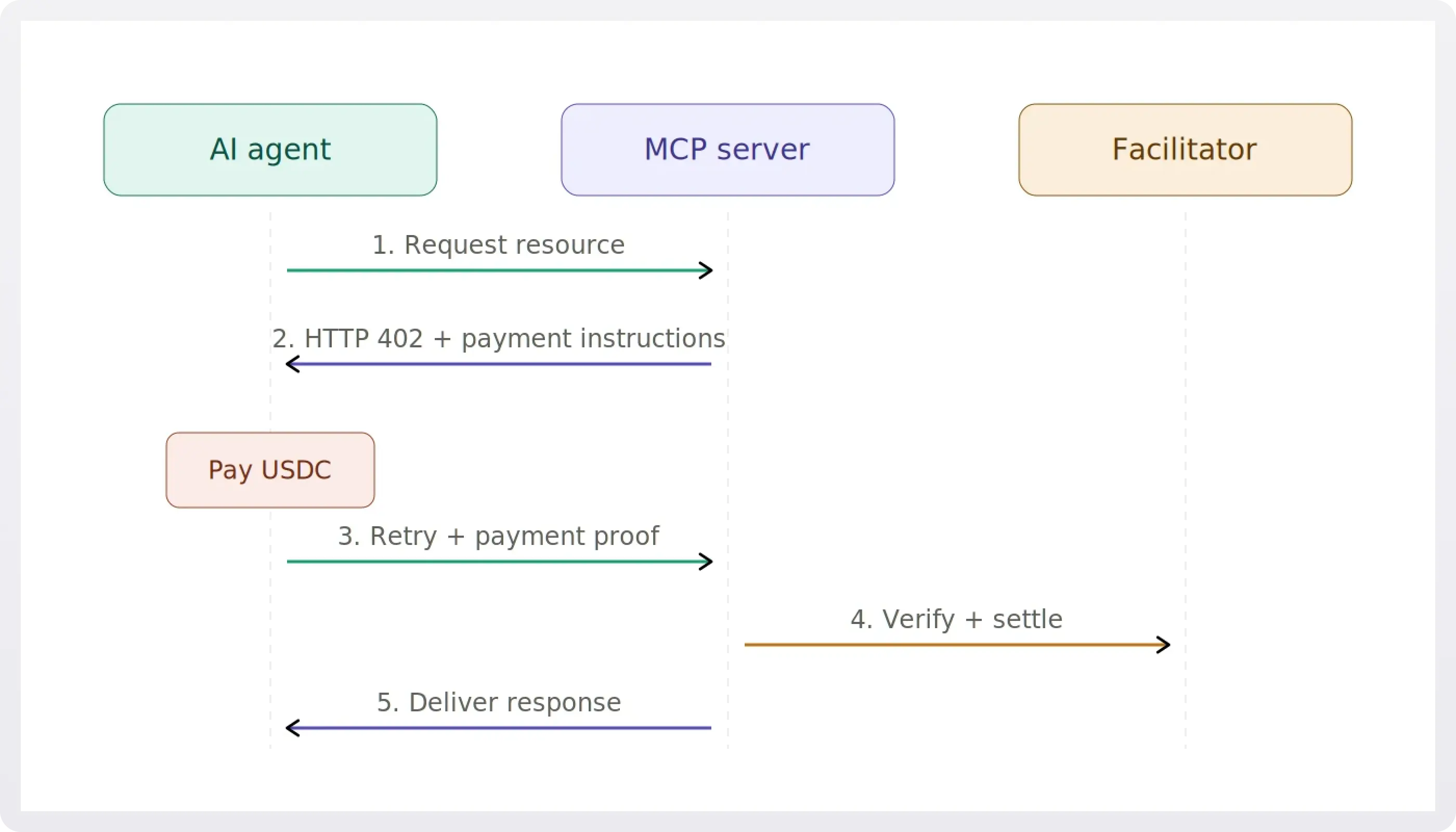

Traditional compliance is a post-hoc audit. You check the user, then you allow the service. x402 endpoints flip this by making compliance a pre-condition for payment. The HTTP 402 status code isn't just an error; it's a gate. If the agent hasn't verified the counterparty's identity through the x402 endpoint, the payment fails before it clears. This embeds regulatory checks directly into the payment flow, turning legal requirements into technical constraints.

x402 shifts compliance from a post-hoc audit to a pre-condition for service delivery, embedding regulatory checks into the payment flow itself.

This infrastructure is critical for institutional adoption. As noted by legal frameworks discussing the x402 protocol, the convergence of stablecoins and blockchain settlement requires regulatory clarity to scale 1. By enforcing KYC/AML checks at the endpoint level, developers ensure that agent commerce doesn't just work technically, but remains viable legally.

How x402 enforces KYC at the endpoint

The x402 protocol shifts identity verification from a passive database check to an active, cryptographic gate. Instead of relying on a central server to say "yes" or "no," the endpoint itself demands a signed PaymentPayload that proves the buyer has both the funds and the verified identity required to access the resource.

This mechanism works by embedding compliance into the transaction flow. When an API receives a request, it first checks for a valid x402 signature. If the payload is missing or invalid, the API returns an HTTP 402 Payment Required status. This isn't just a rejection; it's a request for proof. The buyer must then sign a payload that includes metadata about their KYC status—often linked to a decentralized identifier (DID) or a zero-knowledge proof—before the API grants access.

The beauty of this approach is that it removes the need for the API provider to store sensitive user data. The verification happens on-chain or via a trusted facilitator, and the API only sees the result: a valid, signed token that says "this user is verified." This reduces liability and simplifies compliance, as the API provider doesn't need to manage KYC databases or handle sensitive personal information.

The client sends a standard HTTP request to the API endpoint. The server immediately checks for the presence of an x402 header containing a signed PaymentPayload. If no payload is present, the server responds with a 402 status code, signaling that payment and verification are required.

Once a payload is submitted, the API validates the cryptographic signature. It checks that the payload was signed by the buyer's wallet and that the included metadata—such as KYC status or transaction details—matches the expected format. This step ensures the request is authentic and hasn't been tampered with.

The API verifies the KYC/AML status embedded in the payload. This might involve checking a zero-knowledge proof against a known verifier or confirming that the buyer's address is not on a sanctions list. If the compliance check fails, the request is denied with a specific error code indicating the reason.

If the signature is valid and the compliance check passes, the API grants access to the requested resource. The transaction is then settled on-chain, and the API provider receives the payment. This completes the loop, ensuring that only verified, paying users can access the service.

This flow ensures that every request is tied to a verified identity and a completed transaction. By using x402, API providers can enforce strict KYC/AML policies without becoming custodians of user data, reducing risk and simplifying regulatory compliance.

Integrating KYC checks into the payment flow

Before an AI agent can trigger a payment, you need to ensure the counterparty is who they say they are. This is where x402 endpoints for KYC/AML checks bridge the gap between automated commerce and regulatory compliance. The goal is simple: verify the user, then gate the payment.

We’ll use Fenergo as our example provider for identity verification, but the logic applies to any KYC vendor. The process involves three main steps: setting up the verification endpoint, handling the response, and enforcing the payment gate.

Step 1: Set up the verification endpoint

First, create a dedicated endpoint on your x402-enabled API that handles KYC verification requests. This endpoint should accept a user identifier and return a verification status. When an AI agent calls your API, it should first hit this verification endpoint. If the user is verified, the agent can proceed to the payment endpoint. If not, the agent receives an error and stops.

Step 2: Handle the response

Once the verification endpoint returns a status, you need to handle the response. If the user is verified, you can proceed to the payment endpoint. If not, you should return an error message that explains why the payment was blocked. This could be due to a failed identity check, a suspicious transaction, or a missing document.

Step 3: Enforce the payment gate

The final step is to enforce the payment gate. This means that the payment endpoint should only accept requests from verified users. If an unverified user tries to make a payment, the endpoint should reject the request and return an error. This ensures that only compliant users can trigger payments.

Comparison: Traditional API vs. x402

Traditional API key authentication is simple but lacks the compliance depth needed for financial transactions. x402 payment-gated authentication adds a layer of verification that ensures only verified agents can trigger payments.

| Feature | Traditional API | x402 Payment-Gated |

|---|---|---|

| Authentication | API Key | Payment + KYC |

| Compliance | None | Built-in |

| Fraud Protection | Low | High |

Why this matters

Integrating KYC checks into your payment flow is not just about compliance. It’s about building trust. When users know that your API is secure and compliant, they are more likely to use it. This is especially important for AI agents, which often operate in high-risk environments.

Avoiding common compliance pitfalls

When building x402 endpoints for KYC/AML checks, the technical implementation is only half the battle. The other half is navigating the specific risks inherent to agent commerce. If your integration treats compliance as an afterthought, you expose your business to malicious facilitators, data privacy leaks, and regulatory penalties.

Malicious Facilitators and Trust

In decentralized agent workflows, a malicious facilitator might attempt to intercept KYC data or manipulate settlement records. x402 mitigates this by ensuring that every PaymentPayload is signed by the buyer and settled directly on-chain. This cryptographic proof prevents intermediaries from lying about settlement status or stealing funds during the verification process. Without this layer, your KYC endpoint becomes a vulnerable choke point rather than a secure gate.

Data Privacy Leaks

KYC requires sensitive personal information, but transmitting this data through unencrypted or poorly secured channels creates massive liability. Ensure your x402 endpoint enforces strict data minimization principles. Only collect the fields necessary for the specific AML tier required. Use end-to-end encryption for all data in transit between the agent, the KYC provider, and your backend. Never log full PII (Personally Identifiable Information) in your API response bodies or server logs.

End-to-End AML Standards

Compliance isn't a one-time check; it's a continuous process. Your x402 integration must support the full end-to-end KYC lifecycle: Customer Identification, Due Diligence, Enhanced Due Diligence for high-risk users, and ongoing monitoring. If your endpoint returns a "verified" status but doesn't flag subsequent suspicious activity, you are non-compliant. Integrate real-time transaction monitoring to detect patterns that suggest money laundering, ensuring your x402 endpoints remain robust against evolving regulatory standards.

Verify your x402 KYC implementation

Before you go live, you need to ensure your x402 endpoints for KYC/AML checks handle both the technical payment flow and the regulatory verification correctly. The goal is to prevent false positives and ensure that identity data is processed securely alongside on-chain settlement.

Confirm that your API returns a 402 Payment Required status when a user lacks valid identity credentials. The response body must include a valid PaymentPayload that the client can sign. Test this with a mock KYC provider to ensure the endpoint correctly gates access until verification is complete.

Verify that the buyer’s signed PaymentPayload is correctly parsed and settled on-chain. According to x402 documentation, every payload is signed by the buyer to prevent facilitator fraud. Ensure your backend validates the signature before releasing the KYC status to the client.

Identity providers can experience downtime. Implement a retry mechanism or a fallback state in your API. If the KYC provider is unreachable, your x402 endpoint should return a clear error code rather than hanging, allowing the client to handle the temporary failure gracefully.

Test how your system handles invalid IDs, expired documents, or mismatched biometric data. Ensure that error responses are detailed enough for the client to guide the user but do not leak sensitive internal logic. A robust error handling strategy is essential for maintaining user trust during the verification process.

Once these steps are verified, your integration should be ready for production. Regularly monitor your on-chain settlement logs to ensure that payments and identity verifications remain in sync.

Frequently asked questions about x402 KYC

x402 enables automated, machine-readable identity verification, but it relies on established compliance frameworks. Understanding how these frameworks map to API calls clarifies the integration process.

No comments yet. Be the first to share your thoughts!