Why x402 fits regulated agent commerce

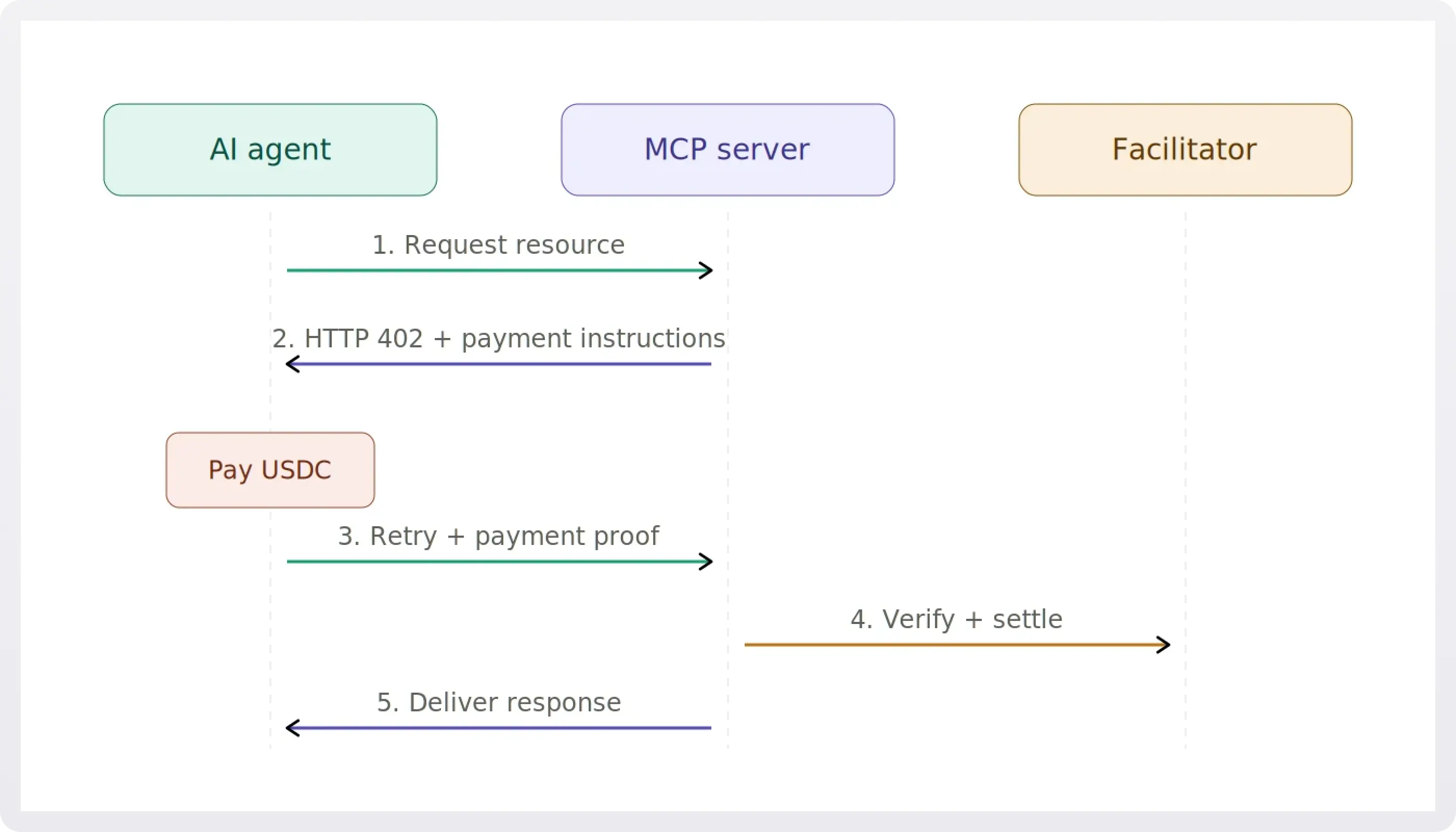

The x402 protocol redefines the HTTP 402 status code from a simple payment gate into a compliance layer. For regulated agent commerce, this shift is critical. It allows servers to enforce Know Your Customer (KYC) and Anti-Money Laundering (AML) checks as a strict prerequisite for transaction execution, rather than an afterthought.

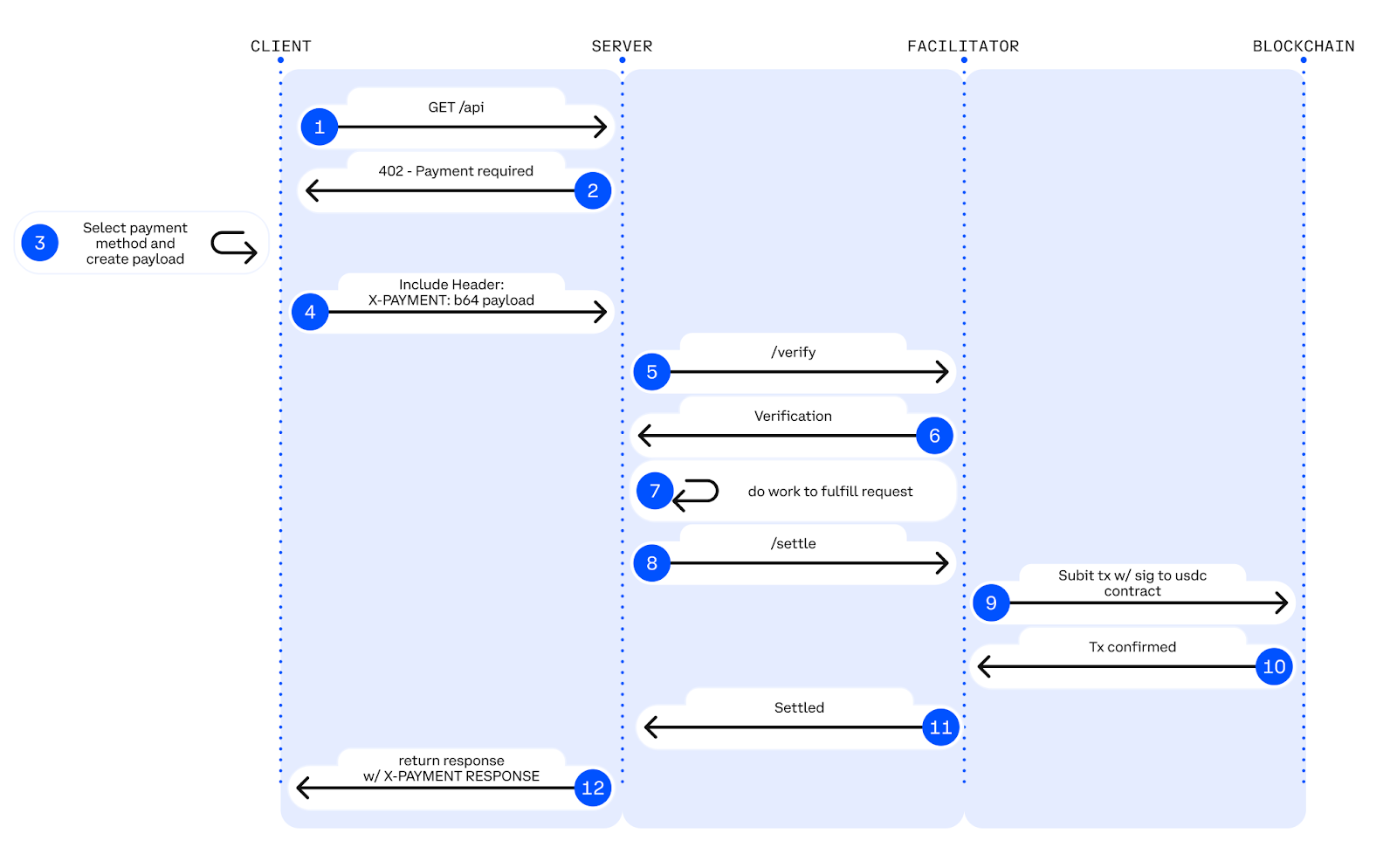

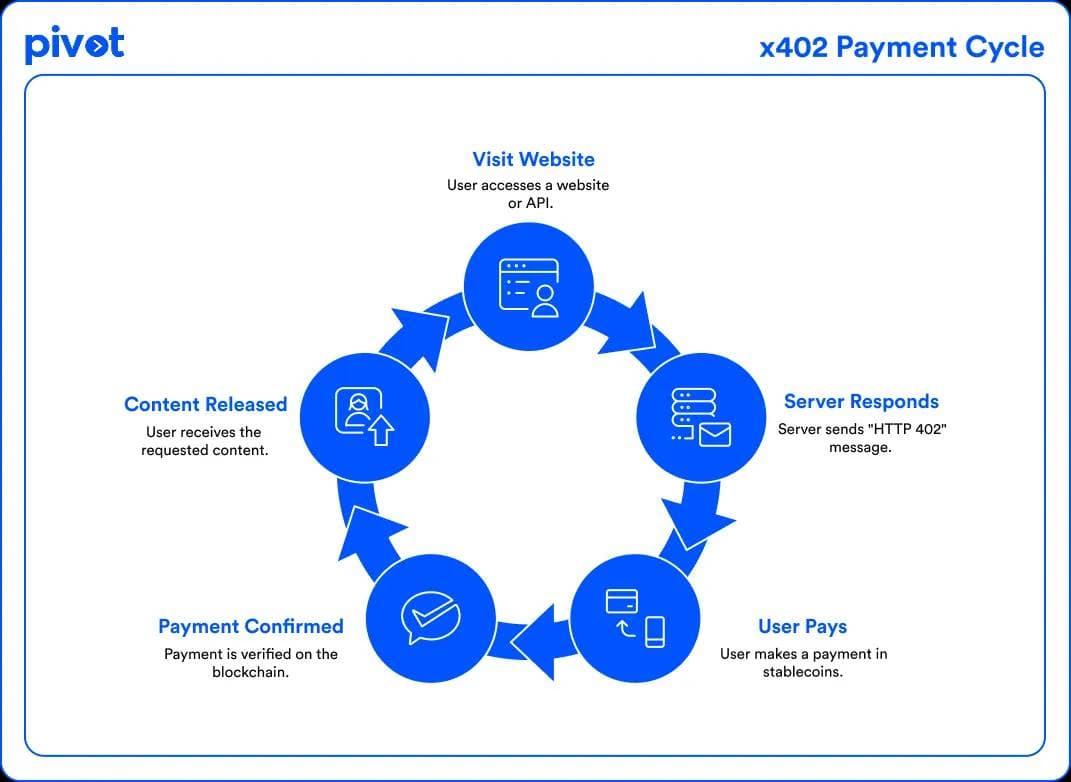

Traditional payment processors often handle compliance separately from the transaction flow. x402 integrates these steps. When an agent requests a service, the server responds with a 402 status. This response can include a challenge requiring the agent to prove its identity or regulatory standing before the payment is processed. This atomic verification ensures that only compliant agents can complete the transaction.

This approach aligns with the technical implementations seen in official documentation from Stripe and Concordium. Stripe’s x402 quickstart guide highlights how machine-to-machine transactions can be built with these endpoints in mind. Similarly, Concordium’s integration docs detail how zero-knowledge proofs can be used to verify compliance without exposing sensitive user data, satisfying both privacy and regulatory requirements.

By embedding compliance into the protocol, x402 reduces the risk of non-compliant transactions. It provides a clear, technical framework for developers to build regulated agent commerce systems that are both secure and compliant.

Comparing x402 integration approaches

Implementing x402 for KYC/AML checks isn't a one-size-fits-all scenario. The protocol is flexible, but the way you handle identity verification and settlement depends entirely on the infrastructure you choose. Below, we break down how Concordium, Stripe, and Browserbase approach the same problem with different architectural trade-offs.

| Platform | Identity Method | Settlement Layer | KYC/AML Depth |

|---|---|---|---|

| Concordium | Zero-Knowledge Proofs (ZKPs) | Concordium Mainnet | Native ZK-based compliance proofs |

| Stripe | Traditional account verification | USD/EUR via Stripe Connect | Full KYC/AML via Stripe Identity |

| Browserbase | Session-based (no identity) | USDC on Base | None (anonymized usage) |

Concordium leans heavily into privacy-preserving compliance. By using zero-knowledge proofs, users can prove they meet KYC/AML requirements without revealing their actual identity data to the merchant. This is ideal for high-stakes financial interactions where data minimization is a core requirement. However, it requires a deeper integration with Concordium's specific SDKs and a more complex user experience for proving identity.

Stripe takes the opposite approach, leveraging its existing trust infrastructure. If you're already building a web or mobile app, Stripe's x402 implementation feels familiar. It relies on traditional account verification and Stripe Identity for KYC/AML checks. The trade-off is less privacy; the merchant knows who the customer is. But the developer experience is significantly faster, with less boilerplate code required to handle payments and compliance.

Browserbase offers a third path: anonymity. Built on the x402 protocol, it allows you to pay for automated browser sessions using USDC on Base. There is no KYC/AML integration here because the service doesn't require user identity. This is perfect for web scraping or testing tasks where privacy is paramount and regulatory compliance isn't tied to the individual user. It highlights that x402 isn't just for payments; it's for any machine-to-machine transaction where identity matters.

Building the x402 Endpoint

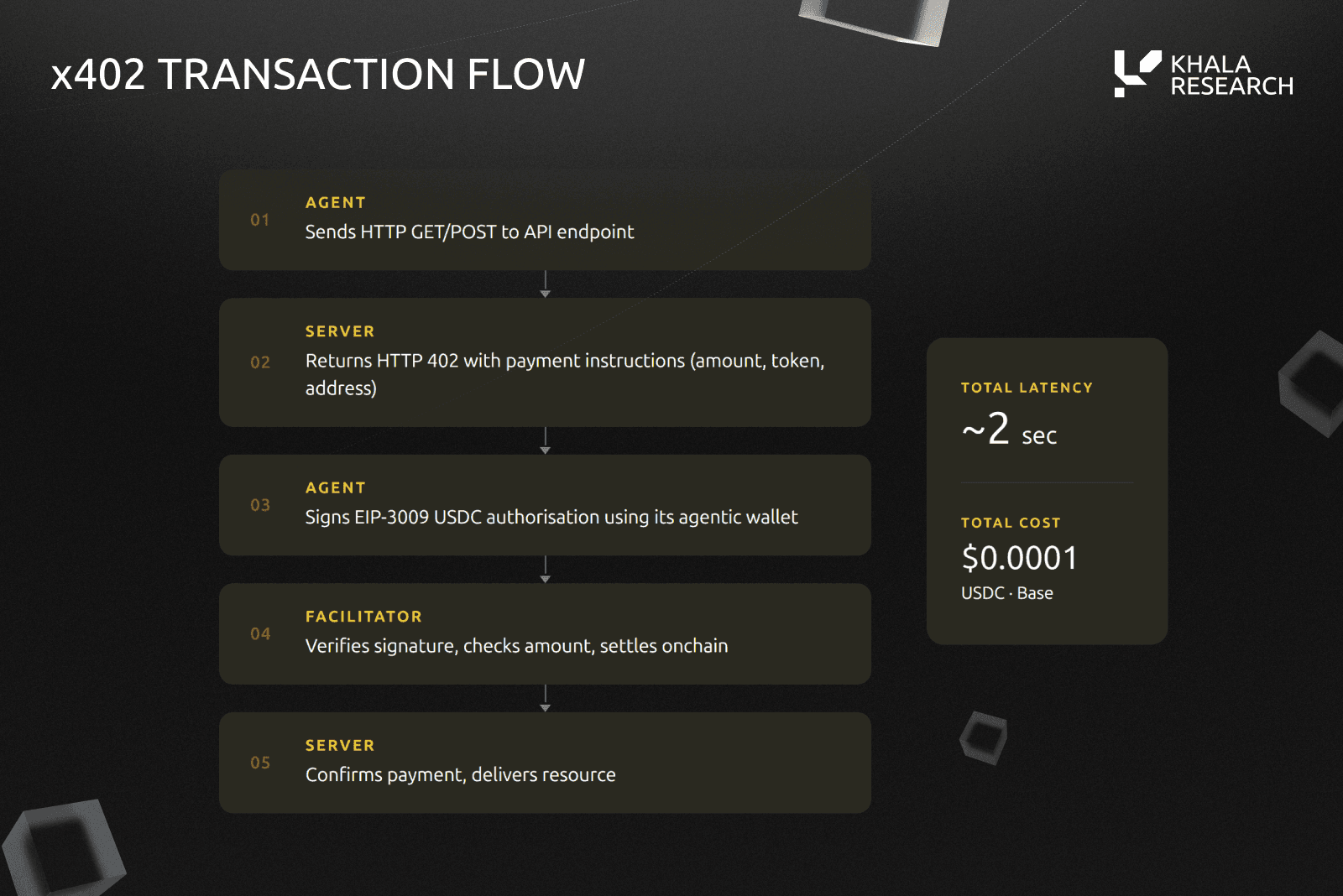

To enforce KYC/AML checks, you need an endpoint that validates identity before processing a payment. The x402 protocol allows machines to pay for services using tokenized transactions, but integrating compliance requires careful handling of verification headers. We will use Stripe’s quickstart as a reference for the API structure, adapting it to include Concordium identity verification steps.

Start by setting up a Node.js or Python server. Install the necessary SDKs for x402 payment processing and your chosen KYC provider. Stripe’s documentation provides a solid baseline for handling the initial HTTP request structure, which you will modify to include identity validation logic before any transaction occurs.

Create a middleware function that intercepts incoming requests. This function must check for valid KYC/AML headers or tokens provided by the client. If the client has not passed identity verification, the endpoint should return a specific x402 error code, preventing the transaction from proceeding until compliance is satisfied.

Connect your middleware to Concordium’s identity verification service. When a request arrives, validate the user’s digital identity against your compliance rules. This step ensures that only verified entities can interact with your API, reducing the risk of money laundering or fraud in machine-to-machine transactions.

Once identity is confirmed, process the x402 payment using the standard Stripe integration. Return a successful response only after both the KYC check and the payment transaction are complete. This ensures that your endpoint is fully compliant with financial regulations while maintaining the speed expected by automated agents.

Handling KYC/AML data with zero-knowledge proofs

Zero-knowledge proofs (ZKPs) allow AI agents to prove compliance without exposing sensitive personally identifiable information (PII). This is critical for high-stakes financial transactions where privacy is as important as security.

Concordium’s implementation of the x402 protocol demonstrates this capability. Users can generate a proof that they meet specific regulatory criteria—such as being over 18 or residing in a permitted jurisdiction—without revealing their actual identity or location data. The x402 endpoint verifies the proof cryptographically, ensuring the agent complies with KYC/AML rules while keeping the user’s private data confidential.

This approach solves the "privacy vs. compliance" dilemma. Instead of sending raw PII to every service, agents only share the minimum necessary proof. This reduces the attack surface for data breaches and aligns with strict data protection regulations like GDPR.

Risk management and compliance checks

x402 endpoints automate payments, but they don’t automate liability. When AI agents handle funds, you need strict operational controls to stay compliant with KYC/AML standards. Think of your endpoint as a gatekeeper: it must verify identity and monitor for suspicious patterns before authorizing a transaction.

1. Integrate KYC Providers

Don’t rely on self-reported data. Integrate with verified identity providers early in the request lifecycle. This ensures that every agent initiating a high-value transaction has passed basic identity checks. Stripe and Concordium offer robust frameworks for this verification step, ensuring that the entity behind the API call is legitimate.

2. Implement Transaction Monitoring

Set up real-time monitoring for anomalous behavior. Look for patterns like rapid, small-value transactions (smurfing) or transfers to known high-risk addresses. Use tools like the Cobo x402 guide to understand common mitigation strategies. Flagging these events early prevents money laundering risks from compounding.

3. Maintain Detailed Records

Regulators require an audit trail. Log every transaction, including the agent’s ID, timestamp, amount, and the KYC verification status. This data is your first line of defense during an audit. Without detailed records, you cannot prove compliance, regardless of your technical safeguards.

4. Adapt to Regulatory Changes

Regulations evolve faster than code. Build a flexible configuration layer in your x402 endpoint that allows you to update AML thresholds and blocked jurisdictions without a full redeployment. This agility is crucial for staying ahead of new financial directives.

Ensure your endpoint calls a verified identity provider before processing any payment. Test this flow with mock identities to confirm that unverified agents are rejected.

If using zero-knowledge proofs for privacy, verify that the proof generation doesn’t bypass KYC requirements. Ensure the proof validates identity without exposing unnecessary personal data.

Implement immutable logging for all transactions. Store agent IDs, timestamps, and amounts. This data is critical for compliance audits and forensic analysis.

Set clear thresholds for manual review. Configure your system to flag transactions exceeding specific limits or those originating from high-risk jurisdictions.

Frequently asked questions about x402 compliance

x402 endpoints for KYC/AML checks sit at the intersection of machine-to-machine payments and regulatory compliance. Here are the most common technical questions developers ask when integrating these systems.

No comments yet. Be the first to share your thoughts!