Set up x402 payment middleware

Before you can route KYC or AML checks through an x402-enabled API, you need to install the necessary dependencies and configure the payment middleware. This setup ensures your API can handle HTTP 402 responses and process crypto payments for sensitive compliance data.

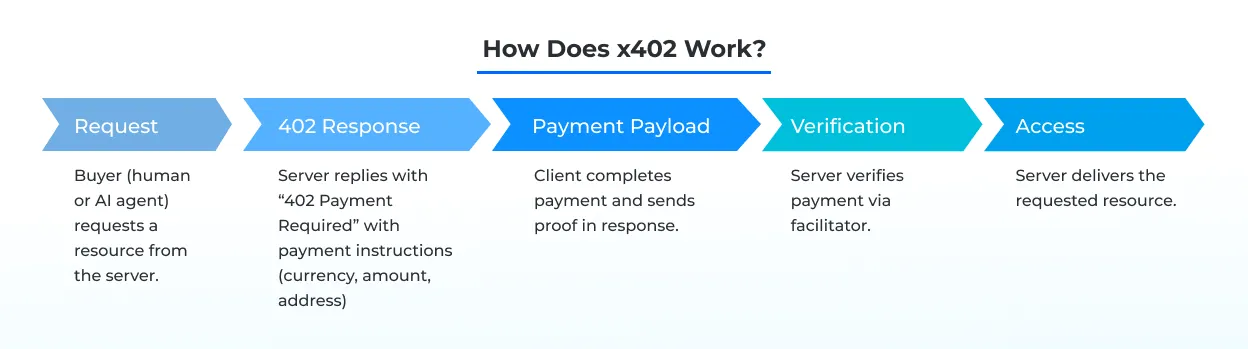

Follow these steps to configure your environment for x402 endpoints for KYC/AML checks.

Start by installing the official x402 SDK in your project directory. This package provides the core functions for generating payment requests and validating transactions. Run npm install @x402/sdk to add it to your dependencies. This step is foundational for any x402 integration.

Next, configure your API middleware to intercept requests that require compliance checks. You will need to set up a handler that checks for the Pay-To header. If the header is missing or invalid, the middleware should return an HTTP 402 status code with a payload containing the payment instructions. This ensures that only paid requests proceed to the KYC/AML verification logic.

Refer to the Coinbase x402 Quickstart for Sellers for detailed code examples on setting up this middleware layer.

Finally, integrate a payment validation module. This module listens for incoming payments on the specified blockchain network and verifies that the transaction is confirmed before releasing the KYC/AML data. You can use a provider like Coinbase Commerce or a direct wallet listener to monitor transaction status. Once confirmed, the middleware updates the request context to allow the API to proceed with the sensitive check.

Integrate KYC verification logic

Embedding identity verification into your API flow ensures that access is granted only after successful KYC checks. This approach aligns with the end-to-end KYC process, which includes Customer Identification Program (CIP), Customer Due Diligence (CDD), and ongoing monitoring for suspicious activity. By treating KYC as a gatekeeper, you prevent unauthorized access and maintain compliance with AML regulations.

Create a dedicated endpoint for identity verification. This endpoint should accept user data and return a verification status. Use x402-compliant endpoints to ensure seamless integration with your existing infrastructure.

Integrate a KYC provider API to validate user identity. This step typically involves verifying government-issued IDs, biometric data, or other identity documents. Ensure the validation process is secure and complies with data protection regulations.

Once verification is complete, update the user's status in your system. Grant access only if the KYC check passes. If verification fails, deny access and provide clear feedback to the user. This step ensures that only verified users can interact with your platform.

Implement ongoing monitoring to detect suspicious activity. This includes tracking transaction patterns, flagging unusual behavior, and updating user profiles as needed. Regular audits help maintain compliance and protect against financial crimes.

Structure payment schemes for access

When building KYC and AML endpoints, you need to decide how the client pays for each verification step. The x402 protocol supports two primary billing models: exact and upto. Choosing the right one depends on whether your verification costs are fixed or variable.

Exact payment model

The exact model requires the client to send a precise amount of crypto to unlock a specific check. This works well for standardized, low-cost verifications like basic identity validation where the backend cost is predictable. The transaction is simple: the client pays the set price, and the endpoint responds immediately.

Upto payment model

The upto model allows the client to send a maximum amount, with the endpoint charging only what is necessary. This is ideal for complex AML checks that may require multiple data sources or deeper background scans. If a check costs less than the sent amount, the protocol handles the refund or credit, ensuring the client doesn't overpay for simpler cases.

Comparison of billing models

Use the table below to decide which scheme fits your API's pricing strategy.

| Feature | Exact Payment | Upto Payment |

|---|---|---|

| Cost Predictability | Fixed per request | Variable based on depth |

| Best For | Standard KYC checks | Complex AML screening |

| Client Risk | Pays exact fee upfront | Pays max, gets refund |

| Implementation | Simple fixed price | Requires refund logic |

Validate compliance and security

Before you let x402 endpoints go live, you need to ensure they handle the heavy lifting of financial regulation. The protocol itself is just a payment layer; the compliance logic lives in how you configure the checks. If you skip this step, you aren't just risking a broken integration—you are exposing your infrastructure to BSA/AML violations and sanctions breaches.

Think of your endpoint as a gatekeeper. It doesn't just accept tokens; it validates the identity behind them. You must implement real-time screening against the Office of Foreign Assets Control (OFAC) list. This is non-negotiable. If a transaction involves a sanctioned entity, your endpoint must reject it immediately. Do not rely on batch processing for this. The risk window is too small.

Beyond sanctions, you need to integrate Know Your Transaction (KYT) screening. While KYC verifies who the user is, KYT monitors where the funds are going. This helps you detect if incoming assets have ties to mixers, darknet markets, or other high-risk addresses. Combining OFAC checks with KYT screening creates a two-layer defense that mitigates legal risk before the money ever touches your books.

To help you prepare, here is a concise compliance checklist for your pre-launch review:

-

Verify OFAC list integration is active and updated daily

-

Confirm KYT screening thresholds are set for high-risk addresses

-

Ensure transaction logs are immutable and auditable

-

Test rejection flows for sanctioned entities

-

Document the decision logic for compliance officers

This checklist is a starting point. Your specific risk appetite and jurisdiction may require additional steps. But if these boxes are not checked, you are not ready to launch.

Frequently asked: what to check next

What is the end-to-end KYC process in AML?

The end-to-end KYC process typically follows four stages: Customer Identification Program (CIP), Customer Due Diligence (CDD), Enhanced Due Diligence (EDD) for high-risk customers, and ongoing monitoring for suspicious activity. Non-compliance with these stages can result in severe penalties, so integrating these checks into your x402 endpoint workflow is essential for maintaining regulatory standing.

What is the difference between AML and KYC checks?

AML is a broad framework designed to combat financial crimes, including money laundering and terrorist financing. KYC, on the other hand, focuses specifically on verifying customer identity and intent during onboarding and maintaining due diligence throughout the business relationship. While KYC is the initial gate, AML is the continuous surveillance system that operates behind it.

How do x402 endpoints simplify KYC/AML integration?

x402 endpoints allow developers to embed compliance checks directly into the payment flow, reducing friction for users. By handling verification at the point of transaction, you can ensure that only verified users complete high-value actions, streamlining the overall user experience while maintaining strict adherence to AML regulations.

What data is required for a standard KYC check?

A standard KYC check usually requires government-issued identification, proof of address, and sometimes biometric data for enhanced verification. Ensure your x402 implementation securely collects and transmits this data to your compliance provider, keeping user privacy and data protection laws in mind.

Can x402 endpoints handle real-time AML screening?

Yes, x402 endpoints can be configured to perform real-time AML screening by integrating with global sanctions lists and watchlists. This ensures that transactions are blocked or flagged immediately if a user matches a known high-risk profile, preventing potential financial crimes before they occur.

No comments yet. Be the first to share your thoughts!