Why x402 needs compliance checks

Standard KYC/AML flows rely on human-led API calls where a user explicitly approves a transaction. In agent-to-agent commerce, these interactions are autonomous and often occur at machine speed. This shift creates a unique risk profile: traditional compliance checks are too slow for the latency requirements of AI agents, yet they are essential for preventing illicit activity.

The x402 protocol addresses this by embedding compliance directly into the payment layer. Instead of a separate, lagging verification step, x402 allows for zero-knowledge proofs (ZKPs) that verify identity and regulatory status without exposing sensitive personal data [src-serp-1]. This means an AI agent can prove it is KYC-compliant before a transaction even begins, enabling seamless yet secure agent commerce.

Without this integration, high-value agent transactions remain vulnerable to money laundering and regulatory scrutiny. Implementing x402-specific compliance ensures that AI agents can operate within legal boundaries while maintaining the speed and efficiency required for automated economic activity [src-serp-5].

Architecting the x402 payment flow

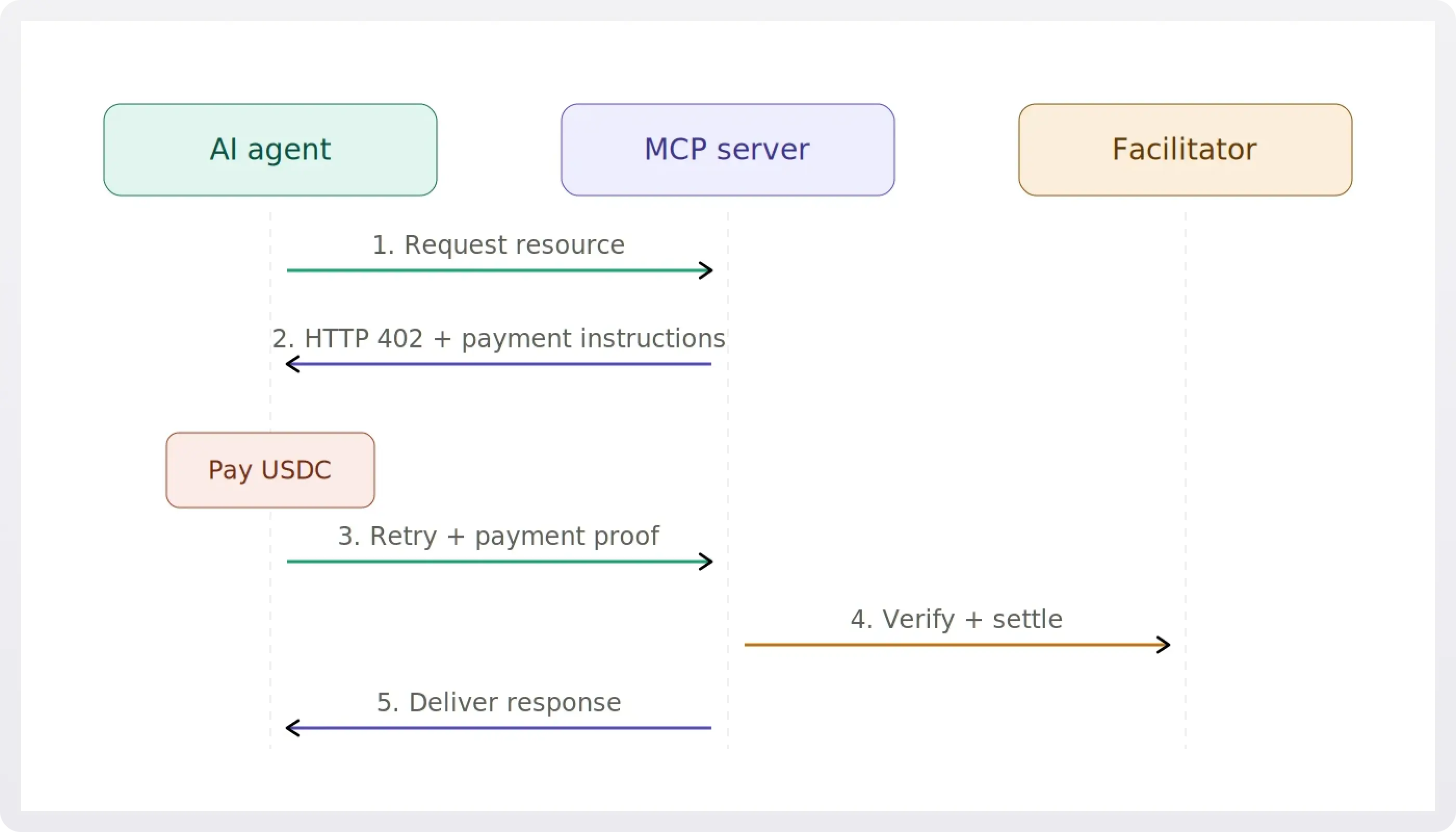

Before implementing the KYC/AML verification steps, you must define how the Client, Server, and Facilitator interact. The x402 protocol relies on a specific handshake where payment intent travels inside an HTTP header before any sensitive data or content is released.

This flow ensures that machine-to-machine transactions are settled before the API responds. The following steps outline the standard sequence for a compliant endpoint.

The Client (an AI agent or script) sends an HTTP GET or POST request to the Server. Crucially, it includes the Authorization header with a valid x402 payment token. This token proves the Client has already transferred the required funds to the designated payment address.

Upon receiving the request, the Server intercepts the Authorization header. It validates the token against the blockchain or payment processor (such as Stripe) to confirm the transaction is final and irreversible. If the payment is missing or invalid, the Server returns a 402 Payment Required error immediately.

In more complex setups, a Facilitator (like a payment gateway or middleware) handles the verification logic. The Server delegates the check to the Facilitator, which ensures the KYC/AML checks are satisfied alongside the payment. This step prevents unauthorized access to sensitive user data.

Once payment is confirmed, the Server processes the request. For KYC/AML endpoints, this means returning the verification status or the requested document. The response is sent only after the financial and compliance layers are satisfied, ensuring a secure and auditable transaction.

This sequence transforms a standard API call into a secure, paid transaction. By embedding payment intent in the header, you eliminate the need for separate checkout flows, making it ideal for automated agent commerce.

Integrating KYC/AML checks into endpoints

To run secure agent commerce, your x402 endpoints must verify user identity before releasing any digital content. This integration acts as the gatekeeper, ensuring that only compliant users can trigger transactions. You can achieve this verification using Zero-Knowledge Proofs (ZKPs) for privacy-preserving checks or by integrating external identity providers.

The following steps outline how to embed this verification middleware into your x402 transaction lifecycle. This approach ensures that compliance checks happen before payment processing, reducing the risk of fraudulent or non-compliant transactions.

Before writing code, determine whether you need full identity verification or just a proof of eligibility. For most KYC/AML applications, you need to verify age, jurisdiction, or sanction list status. ZKPs allow users to prove they meet these criteria without revealing their actual identity. If you choose external providers, identify which ones support the specific data points you require.

Create a middleware function that intercepts incoming x402 requests. This function should check for a valid identity token or ZKP signature. If the user is not verified, the middleware should return a 403 Forbidden response immediately. This prevents unnecessary computation or resource usage on unverified agents.

Connect your middleware to the x402 gateway. When a request arrives, the gateway passes the identity data to your middleware. If the middleware returns a success signal, the gateway proceeds to process the payment and release the content. This ensures that the transaction is both paid and compliant.

Implement clear error handling for failed verifications. If a user fails a KYC check, return a specific error code that explains the issue. This helps users understand why their transaction was rejected and allows them to take corrective action, such as submitting additional documentation.

Use test environments to simulate various user scenarios. Verify that verified users can access content and unverified users are blocked. Test edge cases, such as expired tokens or invalid ZKP proofs, to ensure your system is robust. Concordium’s official documentation provides detailed examples of ZKP integration that you can adapt for your specific use case.

By following these steps, you can integrate KYC/AML checks into your x402 endpoints effectively. This ensures that your agent commerce platform remains secure and compliant with regulatory requirements.

Choosing tools for compliant agent commerce

Building an x402 endpoint for KYC/AML checks requires infrastructure that handles both the cryptographic payment flow and the regulatory verification layer. Not all providers support this dual requirement equally. Some focus on the blockchain settlement, while others specialize in identity verification. You need a stack where the payment facilitator and the compliance engine communicate without friction.

The following table compares three common infrastructure options based on their native support for x402 protocols and KYC/AML compliance capabilities.

| Provider | x402 Support | KYC/AML Compliance | Best Use Case |

|---|---|---|---|

| Stripe | Via Bridge/API | Full Suite (Identity, Radar) | Traditional web apps needing fiat/crypto hybrid |

| Concordium | Native (DID-based) | Built-in (Verifiable Credentials) | Privacy-preserving agent-to-agent commerce |

| Cobo | Via Custody API | Enterprise Custody Compliance | Institutional crypto asset management |

Stripe: The Bridge Approach

Stripe does not have a native x402 protocol implementation in its core SDK, but it serves as a critical bridge for agents operating in hybrid environments. Their Identity product handles the KYC/AML checks, while their Treasury or Connect APIs manage the settlement. For an x402 endpoint, you would typically use Stripe to verify the user’s identity before issuing a token or API key that grants access to the x402-gated resource. This is ideal if your agents need to interact with traditional payment rails alongside crypto.

Concordium: Native Compliance

Concordium is built for privacy-preserving compliance, making it a strong candidate for native x402 integration. Its decentralized identity (DID) system allows agents to present verifiable credentials for KYC/AML checks without exposing raw personal data. Since Concordium supports smart contracts that can enforce payment conditions, you can build an x402 endpoint where the smart contract itself checks for a valid KYC credential before releasing the response. This reduces reliance on third-party intermediaries.

Cobo: Institutional Custody

Cobo focuses on enterprise-grade crypto custody and compliance. While it doesn’t natively implement the x402 protocol for public-facing APIs, its compliance tools are robust for high-stakes agent commerce. If your x402 endpoints handle large-value transactions, Cobo’s infrastructure ensures that the underlying assets meet regulatory standards. You would likely integrate Cobo for the asset holding layer while using a separate facilitator for the x402 payment logic.

As an Amazon Associate, we may earn from qualifying purchases.

Common mistakes in x402 implementation

Even with robust zero-knowledge proof (ZKP) verification, deploying x402 endpoints for KYC/AML checks introduces specific operational risks. Developers often focus heavily on the cryptographic handshake while neglecting the compliance logic that must wrap it. Ignoring these nuances can lead to false negatives in identity verification or, worse, regulatory exposure for high-value transactions.

Ignoring Transaction Limits and Velocity Checks

One of the most frequent errors is treating every x402 request as equal. Financial regulations often require tiered due diligence based on transaction size or frequency. If your endpoint accepts unlimited micro-transactions without aggregating them, you may bypass thresholds that trigger mandatory KYC reviews.

Implement a local ledger or state tracker that aggregates agent spending over defined windows. If an agent approaches a regulatory threshold, the endpoint should pause and request additional identity proofs before processing further payments. This mirrors the risk-based approach recommended by compliance frameworks for digital asset services.

Poor Error Handling in ZKP Verification

ZKP verification is computationally intensive and prone to edge cases. A common pitfall is returning generic HTTP errors when a proof fails to verify. This makes debugging nearly impossible for agents and can obscure whether the failure was due to a malformed proof, an expired credential, or a network timeout.

Return specific error codes that distinguish between "invalid proof structure" and "credential expired." This allows the agent to prompt the user for a fresh credential rather than failing silently. Refer to the Stripe x402 quickstart for patterns on handling machine-to-machine payment errors gracefully.

Lack of Audit Trails

Compliance is not just about preventing fraud; it is about proving you tried. Many implementations store transaction hashes but omit the context: who initiated the request, what KYC tier was verified, and when the ZKP was checked. Without this metadata, you cannot reconstruct the compliance story during an audit.

Ensure every successful x402 response logs the necessary compliance data. This includes the verified identity attributes (without storing raw PII) and the timestamp of the proof verification. This trail is your primary defense if regulators question the integrity of your agent commerce flow.

Pre-launch Compliance Checklist

Before moving your x402 endpoints to production, verify these critical compliance steps:

-

Transaction Aggregation: Confirm your system tracks cumulative agent spending to trigger KYC at defined thresholds.

-

Granular Error Codes: Ensure ZKP failures return specific codes (e.g., invalid_proof, expired_credential) for agent debugging.

-

Immutable Audit Logs: Verify that every transaction logs the verification timestamp, identity tier, and proof hash.

-

Regulatory Monitoring: Set up alerts for changes in local financial regulations affecting machine-to-machine payments.

Frequently asked questions about x402 compliance

Does x402 handle KYC and AML automatically?

No. The x402 protocol provides the technical mechanism for compliance, but it does not perform the checks itself. As noted in the Concordium integration documentation, the system uses Zero-Knowledge Proofs (ZKPs) to allow users to prove they meet specific regulatory criteria without revealing their underlying identity data. You must integrate a compliant provider to issue these proofs.

Can I use x402 for anonymous transactions?

Not if your use case requires KYC/AML compliance. The entire purpose of x402 endpoints in this context is to enforce regulatory standards. While ZKPs protect user privacy by hiding specific details, they still verify that the user has passed a background check. If you need fully anonymous transactions, x402 is not the right tool.

Who is liable if a compliant payment fails a regulatory audit?

Liability depends on your integration. The protocol ensures the transaction can be verified, but it is your responsibility to choose a KYC provider that meets your jurisdiction’s requirements. If you use a provider that issues invalid proofs, or if you fail to implement the x402 endpoint correctly, you may be held responsible for the compliance breach. Always audit your proof verification logic against official standards.

No comments yet. Be the first to share your thoughts!